-

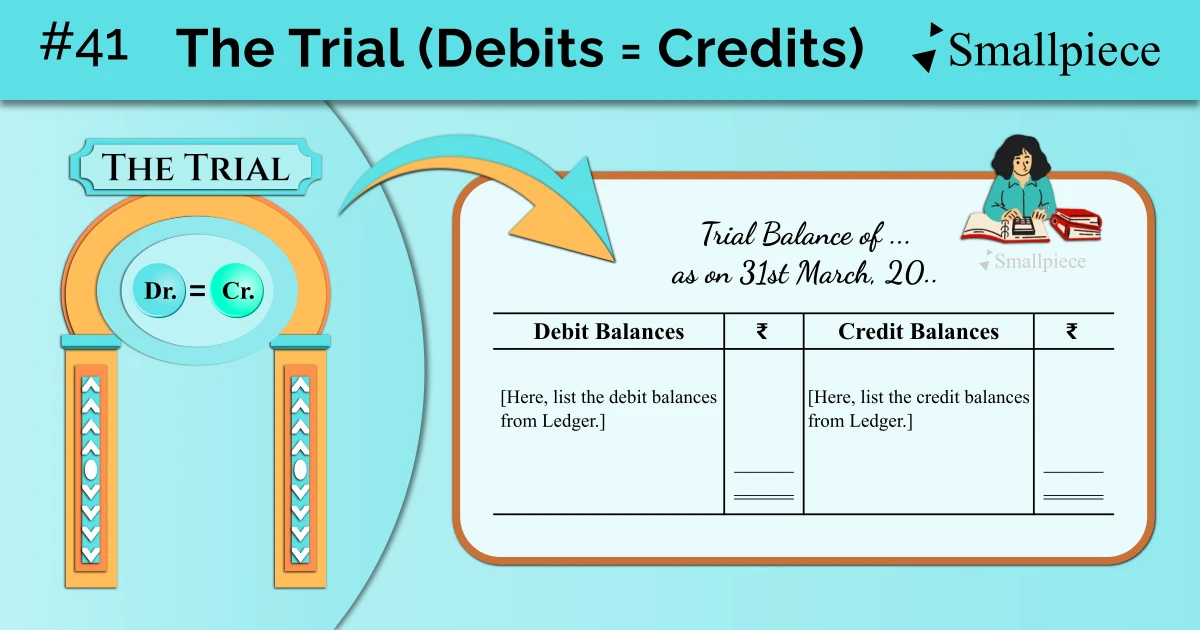

Snippet #41 The Trial

·

The check over Ledger is based on The Dual Aspect Concept i.e., all debits = all credits, the trial all Ledger postings must pass.

-

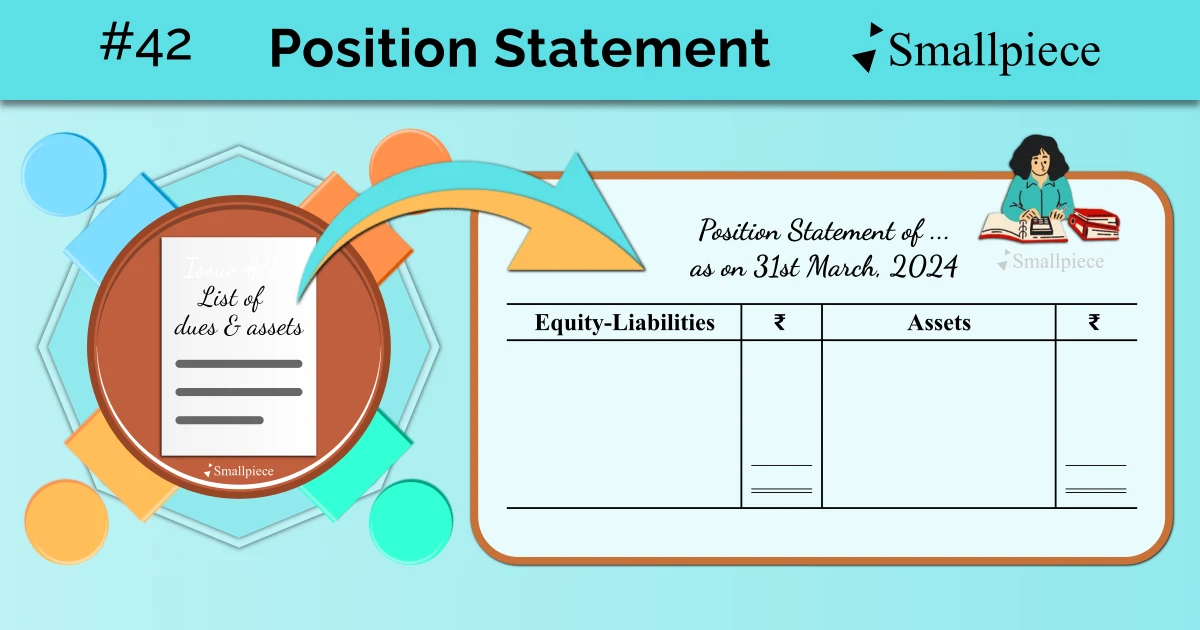

Snippet #42 Position Statement: Answer to the Second Issue

·

To know the “position” of the business, we use a new layout titled the Position Statement, comprising of Equity-Liabilities and Assets.

-

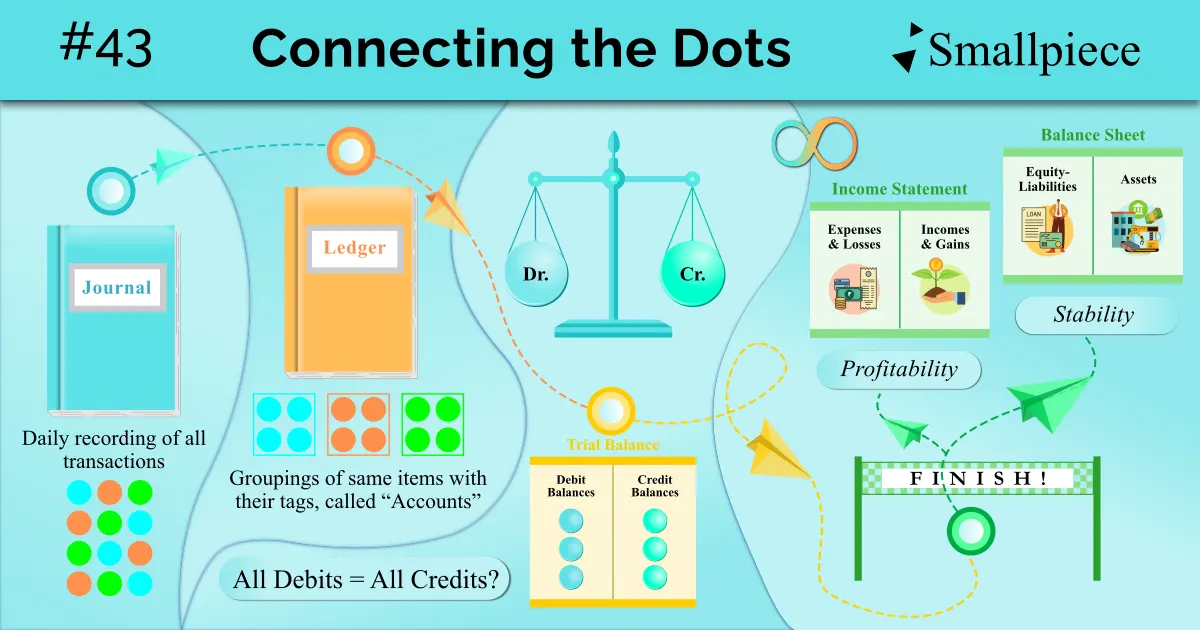

Snippet #43 Connecting the Dots

·

Here, we’ll spend some time not learning anything new but connecting the dots between the concepts we’ve learned earlier.

-

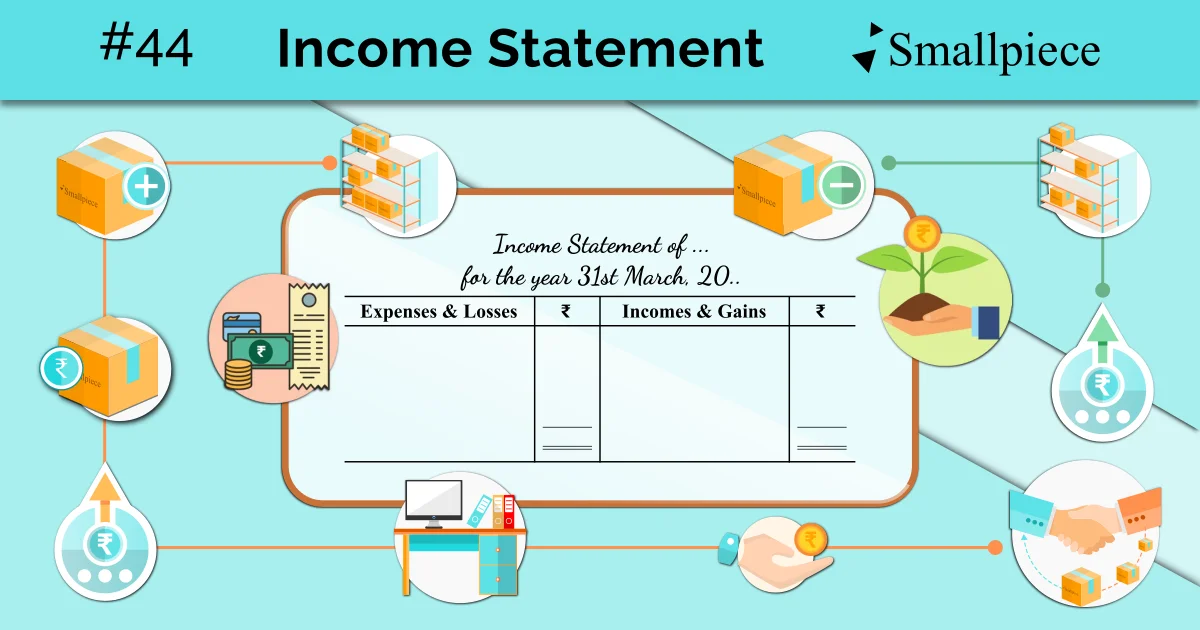

Snippet #44 Income Statement: The Layout & Components

·

Since we’ve gotten the hang of the accounting cycle, it is time we dig deeper into financial statements, starting with the Income Statement.

-

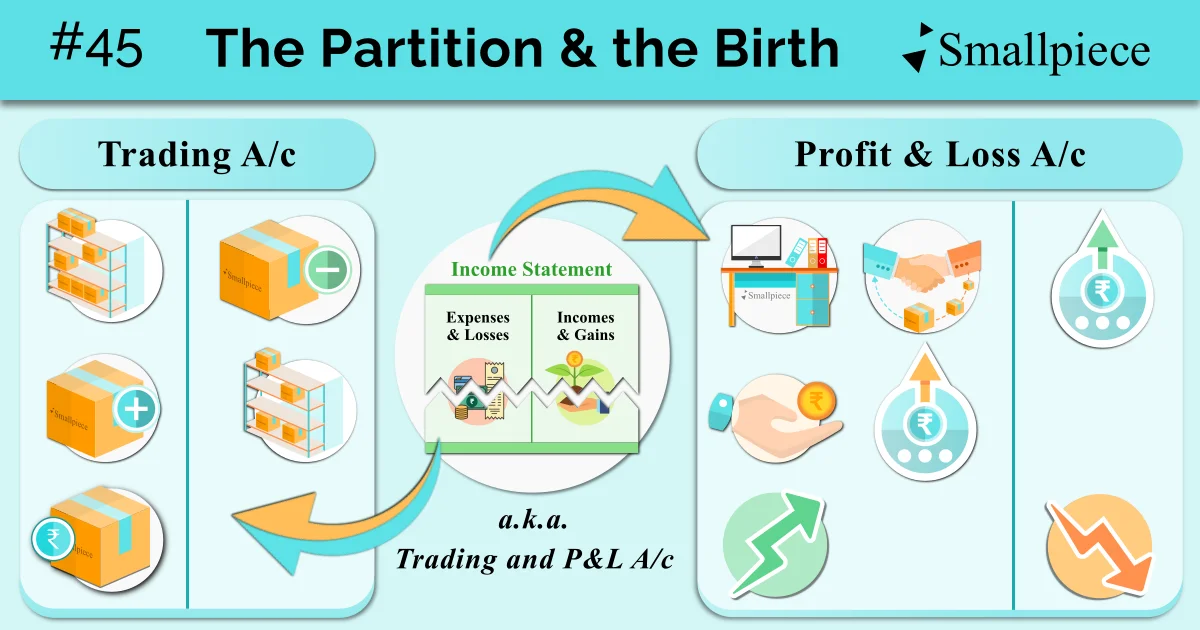

Snippet #45 The Partition & the Birth: Trading and P&L Account

·

The partition of Income Statement, based on the categorisation of expenses, resulted into the birth of Trading account and P&L account.

-

Snippet #46 Prudence: Play it Safe

·

Before discussing the layout of Balance Sheet, we must first discuss one of its components: Reserves & Provisions, born out of the “prudence concept”.

-

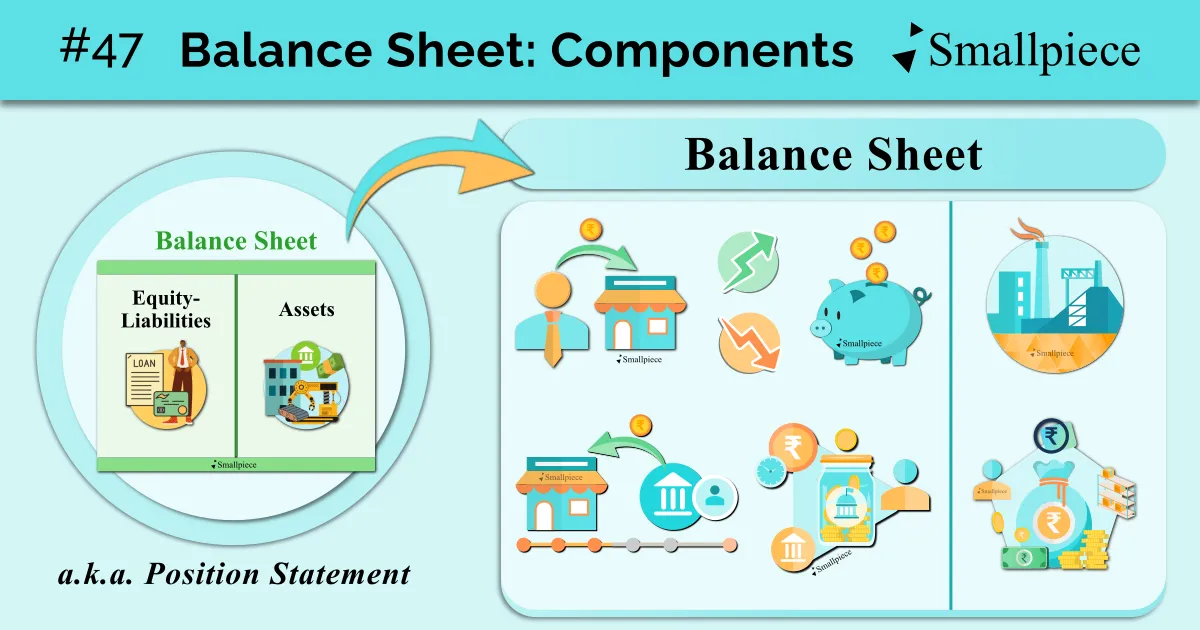

Snippet #47 Balance Sheet: The Layout & Components

·

It is now time that we explore our second financial statement: the Position Statement or what the accounting world calls the “Balance Sheet”.

-

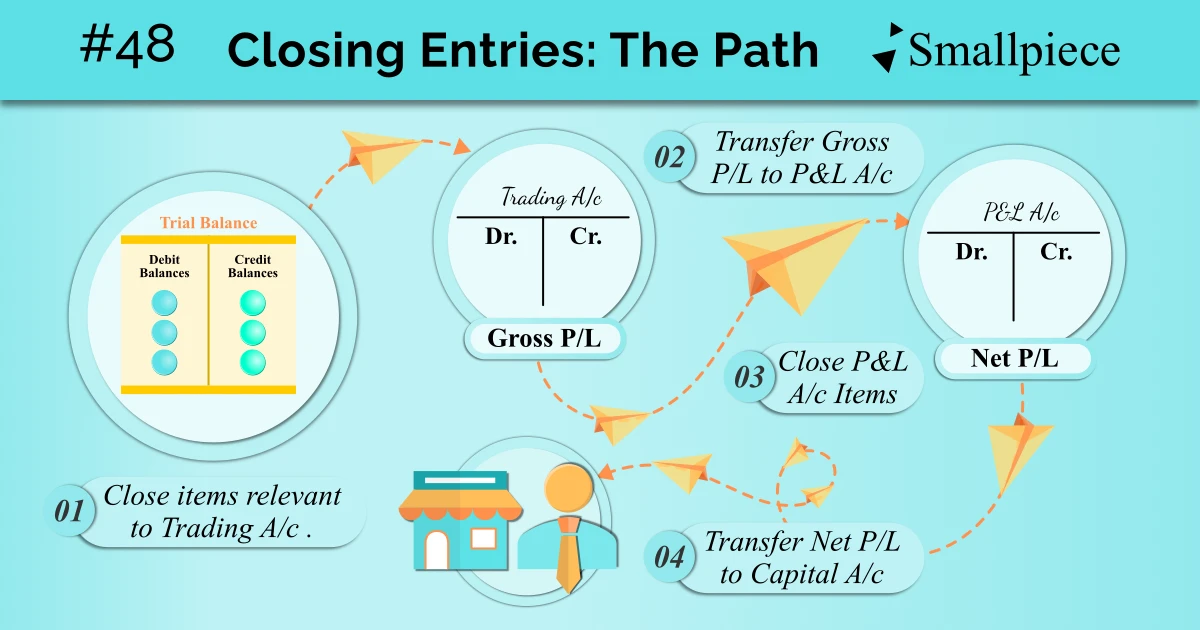

Snippet #48 Closing Entry: The Path to Financial Statements

·

Any recordings made in our financial statements, particularly the Income Statement, require a entry of their own, called the “Closing Entry”.