Here, we’ll spend some time not learning anything new but connecting the dots between the concepts we’ve learned in all our previous meets and discussions.

Knowingly or Unknowingly, we’ve gained a foundational understanding of the accounting cycle, right from journal for daily recording down to financial statements prepared to ascertain the profitability and stability of our business at certain checkpoints in its conceptually endless life.

Position Statement, from the earlier discussion, is another name for “Balance Sheet”, one of the two financial statements that are prepared at the end of the accounting year.

Secondly, the layout we used to calculate our Profit/Loss for Hitesh Traders in all the previous handouts on journal, ledger & trial balance is similar to the format for “Income Statement”, the other statement prepared alongside the Balance Sheet.

Thus, we’ve actually completed the accounting of Hitesh Traders for the accounting year concerned.

In case you forgot, in the earliest introductory snippets, we talked about the definition and goal of accounting:

Accounting is a habit; a habit of keeping a proper record of all business transactions for the businessman to later check the profits and stability of his business.

~ Prithvi J. (2024, Smallpiece)

Not one but two words stand out:

- Profits or, a better word may be Profitability (i.e., the ability of a business to earn profits)

- Stability (i.e., the capacity of a business to repay its debts and stay afloat, while making money for the owners).

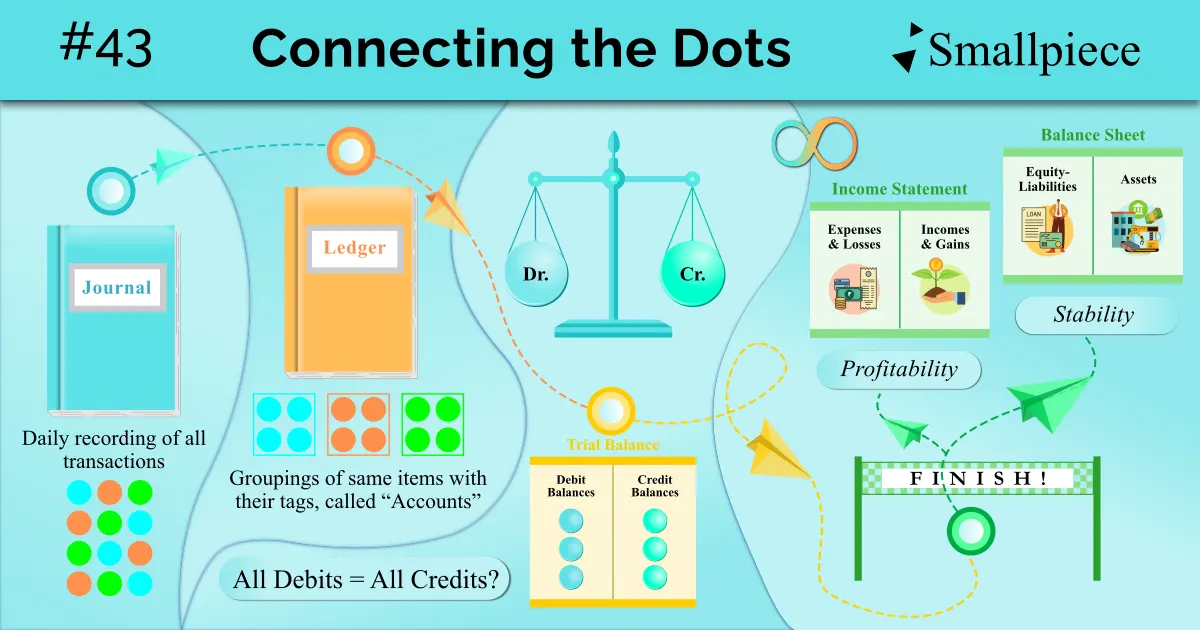

It is to analyse these two aspects of a business that we move through the accounting cycle, starting from Journal where transactions are recorded first of all, on a daily basis.

Then, we move to Ledger where we group same items with their respective tags Debit & Credit and find the balance (i.e., excess of one tag/side over the other) to streamline the profit/loss calculation. Such groupings are what we call “Accounts”.

Then, before we prepare our financial statements, we create a Trial Balance to check the accuracy of our accounting records based on the equality of debits & credits.

Lastly, we prepare our two financial statements. First is the Income Statement where we list the incomes & expenses and find out the Profit/Loss for the period. Then, we move to the second statement: the Balance Sheet where we list the assets & liabilities left at the end of the accounting year. Both the profit and loss belong entirely to the owners and hence, the final profit/loss figure appears alongside Owner’s Capital in the Balance Sheet. Both these statements capture our 4 types of transactions / accounting items: Income, Expense, Equity-Liabilities & Assets and provide a summary of the end amount corresponding to the accounting items under each category.

Below find a graphical mindmap of the entire accounting cycle we’ve discussed just now.

Mind-map

Despite having learnt the position and importance of financial statements in this, we are yet to formally discuss the various items that constitute these statements. Next, we’ll dive into each statement and its components one by one, beginning with the “Income Statement”.

Leave a Reply