I hope that you’ve gone through the summary of accounting concepts provided earlier. The check over Ledger, the answer to the first question, is based on the Dual Aspect Concept.

It states that every transaction has a dual effect on the business. And to record these, we use two tags: Debit & Credit.

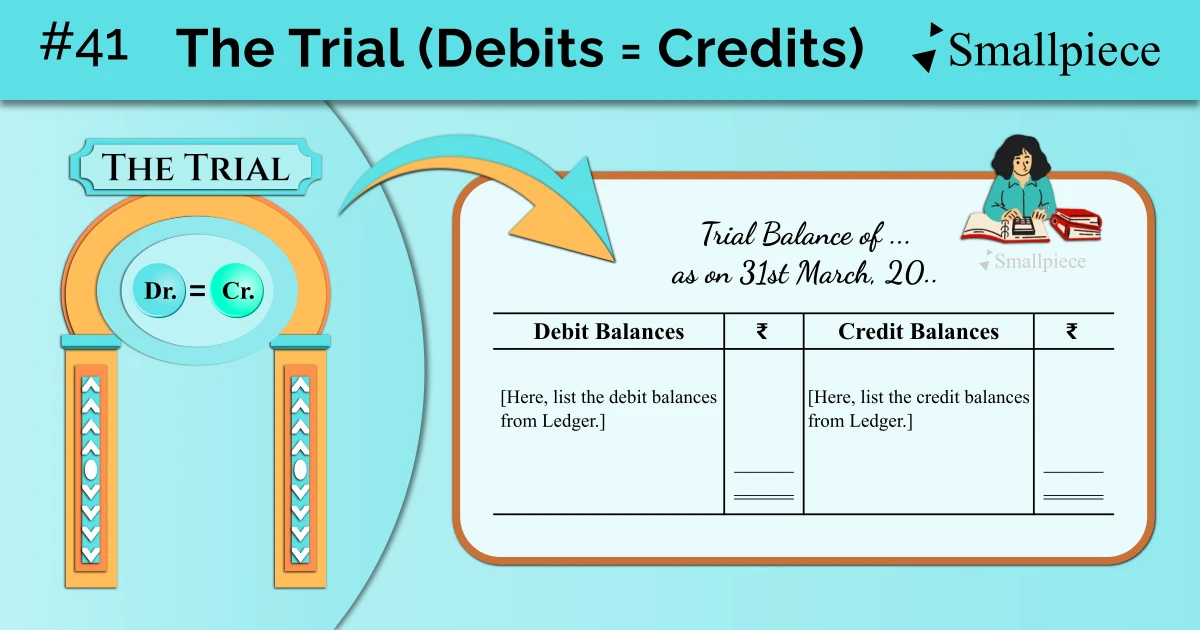

Moreover, Dual Aspect also implies that all debits = all credits.

This equality of debits & credits is the trial / check (whatever you want to call it) that Ledger postings must uphold before we start our P&L calculations.

To undertake this trial, we can use the following format where on one side we’ll list the debit balances from Ledger and on the other, we’ll list the credit balances.

If after listing all the balances correctly, the total of debit balances equals that of credit balances, then we’ve passed the trial and are allowed to go through with our P&L calculations.

Squared-Up Accounts

Outside the ledger postings and balance calculations I’ve made you do (and I hope you’ve taken the time to do so), there is a peculiar case I wish to cover.

What if, in an account, there is no balance? In other words, there is no excess of debit side over credit or vice versa?

Since we know that it is possible for an accounting item to receive both debit & credit tags, it is not entirely impossible, right?

Such accounts, in case you encounter them, are called “Squared-Up Accounts”.

Since they don’t have any balance, they are, by definition, NOT included in trial balance.

But, what could such an accounting item be?

Numerous examples come to mind but a simple one is that of a creditor / supplier. Suppose we purchase some goods from Mr. X on credit (making him a creditor in our accounts) and clear what we owe to him before 31st March, his T-Account in our Ledger will become a squared-up / settled account and will not be listed in the Trial Balance.

An example opposite to this is that of a debtor, who clears his dues before the end of financial year. His account, too, will come up as a squared-up one.

Example Continued

Use the format described above to check whether the Ledger postings of Hitesh Traders are correct or not.

After doing so, do compare your trial balance with the one in the attached document.

And with this small task, I take my leave.

In case you want to practice more, there’s an NCERT text reference with multiple examples. Though it uses a different format, you can simply use the one we discussed here.

Reference

1. Chapter 6 Trial Balance and Rectification of Errors, Till Topic 6.3 (NCERT Class 11 Accountancy 2026-27 Reprint)

https://ncert.nic.in/textbook.php?keac1=6-7

Leave a Reply