Since we’ve gotten the hang of the accounting cycle, it is time we dig deeper into financial statements.

First, we’ll explore the Income Statement.

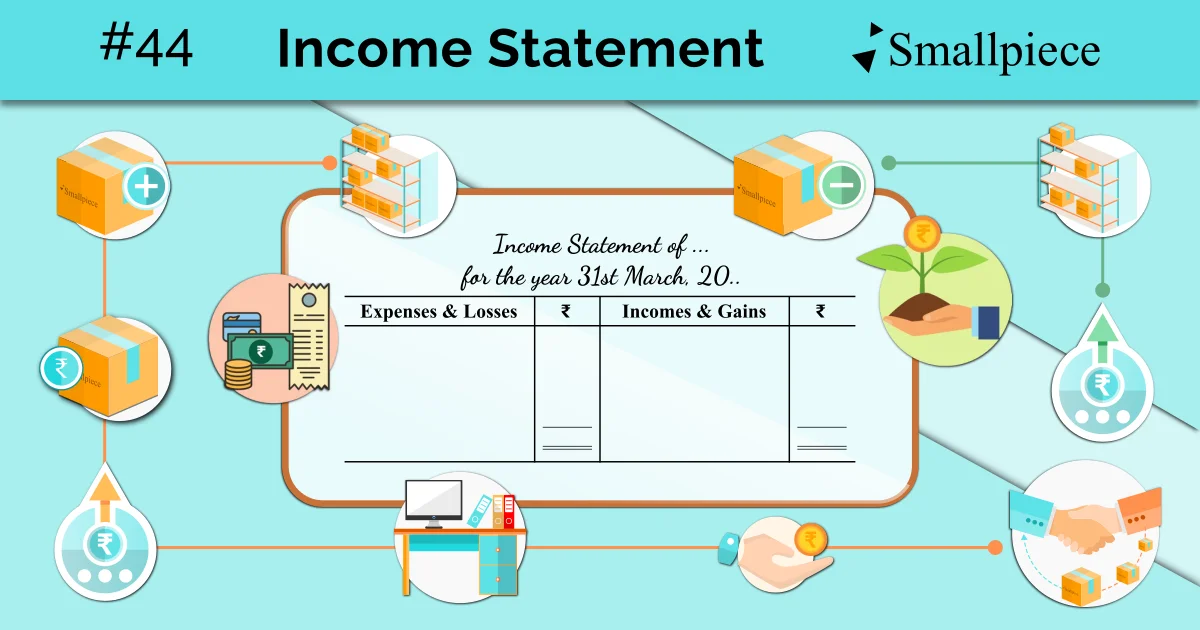

Layout

Income Statement, just like the other things we’ve discussed, is also divided into two sides: One for Expenses and the other for Incomes.

Components

Let us begin with the expenses side and think: What are some expenses that a business incurs in its routine throughout the year?

First would be the amount spent on purchasing goods be it the Purchase Value of Goods (after discount). Then, there’s carriage (i.e., transportation of goods) and if we are a manufacturing firm, there is also factory expenses and wages for labourers. Such expenses associated with the manufacturing / procuring of goods are what we call “Direct Expenses”. And, in case there was some stock carried over from the previous year, that too, comes under the expenses side as “Opening Stock”.

Second: Now that we have our goods, the next thing is selling them to make hard cash. To do so, an additional amount is spent on advertisement, paying for transportation of sold goods from our own pocket (called, Carriage Outward), commission to salesman, etc. Such expenses are called “Selling & Distribution Expenses”.

Third: Regardless of whether you succeed or fail at selling your goods, we are bound to fulfil the interest obligations on our loans borrowed from banks or other financial institutions. Loans, along with our own capital, provide our business with funds which it then uses to compensate for the purchase of assets. In technical language, Loans and Personal Capital are what the business uses to finance (synonym for compensate) the purchase of its assets. Any expenses tied to the raising of these funds (interest on loan, dividend, etc.) are what we call “Financial Expenses”.

To support such core activities of the business, there’s a separate place called the “Office” where there are people who sit full-time on their computer screens, performing the tasks assigned to them. Both this place and the people working hard here have their own expenses, viz. rent, electricity, salary, etc. Such expenses are termed “Office & Administrative Expenses”.

Lastly, there’s a category called “Other Expenses & Losses”, which include depreciation, bad debts, repairs, Loss by fire / theft, etc.

That’s it for the Expenses & Losses side.

Moving on to the Incomes & Gains side, we have:

First, amount received from Sale of Goods.

Second, the amount of stock left at the end of the accounting year or the “adjustment for Closing Stock”. It is something we’ll discuss later on. For now, just keep in mind that keeping opening stock on one and closing stock on the other aids the addition-subtraction necessary to arrive at the profits generated through the sale of goods.

Third: Other Incomes & Gains. These include commission received, rent received, discount received, interest received, etc.

Lastly, with a list of all such expenses and incomes, there’s bound to be a profit / loss which is attributable to the owner who brought the business into being i.e., it is added to / deducted from the Capital account.

Thus, the final layout goes something as follows.

That was it for the Income Statement. Next, we’ll move on to Balance Sheet and its layout… is what I would like to say. But, there are some people who are very much obsessed with the art of breaking down things and analysing them. And it is to accommodate their hobby that our Income Statement had to go undergo a very rough partition, which is what we’ll discuss next.

Academic Reference

NCERT Class 11 Accountancy, 2026-27 Reprint, Chapter 8 Financial Statements-I, Topic 8.4.1

https://ncert.nic.in/textbook.php?keac2=1-2

Leave a Reply