Till now, we’ve learnt Journal & to overcome its shortcomings, we learnt a new book named Ledger where the birth of “Accounts” as we know them, takes place.

But there are a few more questions we’ll address in this chintan shivir 02.

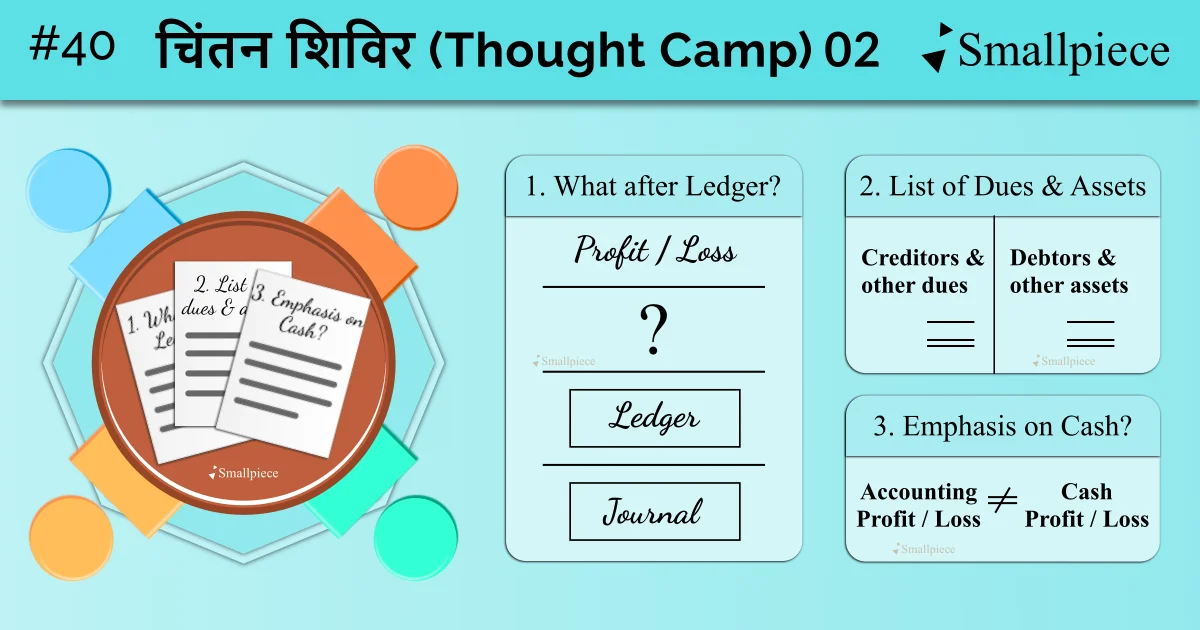

1. Just like how Ledger acts as some sort of a check over journal, shouldn’t Ledger also have some sort of checking mechanism before we move to our P&L calculation?

2. In the documents containing Journal entries & Ledger postings of transactions of Hitesh Traders, I’ve used a format similar to a T-Account to calculate profit / loss on a single page by listing incomes, expenses & other necessary adjustments.

In addition to this one-page P&L calculation, wouldn’t it be better if we had a list of all our debtors-creditors and their dues at one place as well?

3. It is good that we include our receivables and payables in our accounting system. But, shouldn’t we put a little more emphasis on cash? In our calculation, we got a loss of ₹9,975 but our cash balance, as you can see, from our Ledger accounts, is ₹51,650 (i.e., 1,13,550 – 61,900).

For now, let us address the first question i.e., whether the Ledger should have a check before we do our P&L calculations.

The answer is: Of course, it should. And, it does have a check in the real accounting system which is based on simple accounting concepts I’ve introduced to you time & again in our previous discussions. Next is a small review of these concepts. Please go through them or, you can also download a PDF for your convenience from the reference section.

Review of Accounting Concepts

1. Going Concern Concept

It is not possible to estimate the life of a business (i.e., how long a business will carry on).

Thus, for accounting purposes, an assumption is made that a business will continue for a long period of time. It may go on till eternity, who knows?

And this very assumption, is what we call the Going Concern Concept.

But, this assumption led to a problem: If my business will go on for a long time, when should I calculate profits?

2. Accounting Period Concept

To solve Going Concern’s problem, accounting transactions of a business were grouped into equal time periods, referred to as accounting periods, each starting from 1st April to 31st March next year (in India).

The idea of breaking down the life of a business into equal periods, each spanning a year, for accounting purposes came to be known as the Accounting Period Concept or, the Periodicity Concept.

3. Business Entity Concept

In any form of business be it sole proprietorship, partnership, company, etc., it is assumed that the owner and his business are separate entities for accounting purposes.

The owner simply lends his money to a business in the hopes of making more money (or, profits).

It is because of this reason that the accounting treatment of Equity (i.e., Owner’s Funds) is similar to Liabilities (i.e., Borrowed Funds)

4. Money Measurement Concept

Only those business transactions which can be measured in monetary terms should be accounted for.

Put simply, we record a transaction only when it has some sort of price tag attached to it.

Verbal agreements or other cases where a formal price tag is yet to be attached cannot be recorded in our books of accounts.

Examples:

1. Order Placement: A simple verbal agreement does not suffice. This should be recorded only when say, goods are dispatched by the seller or money is received from the customer i.e., when at least one party to the transaction has kept its end of the deal / agreement.

2. Sanction of a Loan: This refers to the approval of a maximum limit the loan applicant can borrow from the bank. And, a mere approval is not accounted for. Any sort of accounting will be done only after the applicant borrows under this limit.

5. Dual Aspect Concept

Any transaction or an exchange, by its very definition, involves two activities i.e., a Give & a Take.

For e.g., on sale of a product, I not only take money from my customer but also give him the requested goods. Similarly, each transaction, be it buy or sell, is looked at from two different viewpoints, both of which should be recorded in our books of accounts.

And, the idea that every transaction has a dual aspect to it & has a two-fold impact on business is what we refer to as the Dual Aspect Concept.

Important Concepts Tied to Dual Aspect Concept:

1. Debits & Credits: Every transaction has a two-fold impact and to record this, two tags were devised; Debit (Dr.) and Credit (Cr.).

2. Accounting Equation: Assets = Equity + Liabilities

This equation is the foundation for understanding journal entries and is used to attach the Dr. & Cr. tags to different accounting items.

6. Accrual Concept

The term accrual originates from the Latin word accrescere— meaning “to become larger.” Another meaning can be “to accumulate.”

When you undertake a credit trade, you either earn the right to receive an income in the future or, accept the responsibility to make a payment in the future. This, in effect, is the same as accumulation of incomes and expenses in the background till the time they are realized i.e., cash is received/paid.

Before the introduction of Accrual Concept, there was no provision to record the accumulated incomes & expenses. But with Accrual Concept, they too were brought under the fold of accounting whereby, incomes receivable in future were recognised as Assets and unpaid expenses were recognised as Liabilities.

Reference

1. Accounting Concepts

2. Topic 2.2 Basic Accounting Concepts (NCERT Class 11 Accountancy 2026-27 Reprint)

https://ncert.nic.in/textbook.php?keac1=2-7

Leave a Reply