Last we discussed that to accommodate the hobby of a few people who like to go into the nitty-gritty of things, our Income Statement had to undergo a partition.

Now, what really happened in the partition?

The activities of a business and particularly, the expenses arising out of the same were divided into two categories:

(A) Trading & Manufacturing Activities, which involves the activities tied to the manufacturing, purchase & sale of goods.

(B) Other Activities, not tied to the trade & manufacturing of goods.

In essence, a distinction was made; separating certain expenses that were “directly” associated with the core offerings of (i.e., goods sold by) the business from the other expenses which only indirectly enable the dealings of the products & services offered.

This separation allowed profits to be calculated at two different levels. At first, only those expenses that comprised the direct “cost” of the goods that the business managed to sell would be deducted from the net sales figure. This would allow owners to ascertain how profitable is their core activity of producing / obtaining goods and selling them for a mark-up.

Then from this first-level profit, those expenses would be deducted which are not directly related to goods. Also at this point, any sort of losses that the business faced and any income earned other than from selling goods would be brought into picture to ascertain the final profit figure.

Giving Names

If you haven’t guessed yet, the partition is what resulted in the categorisation of various expenses into “direct expenses” and “indirect expenses”. Of the various categories of expenses described in the earlier discussions, one was direct expenses that referred to all goods related expenses or simply, any sort of expense that went into creating or acquiring the goods to be put up on sale. These included factory expenses (electricity, water, depreciation), carriage inward, labour wages and so on.

The first-level profit calculated by deducting the value of goods purchased and these direct expenses tied to the same, came to be known as “Gross Profit”.

The final profit figure, arrived at by including indirect expenses in the form of office expenses, selling expenses, etc. and other income comprising of interest earned from investments, came to be known as “Net Profit”.

COGS – The Logic

COGS or, Cost of Goods Sold is the blanket term that covers opening stock, net purchases, closing stock and direct expenses in the Income Statement. Essentially, it covers all items other than sales.

The formula to any profit usually goes: Profit = Selling Price – Cost Price or, Profit = Sales value – Costs Involved

While this may seem simple, we do need to think a little on how to arrive at the cost figure. This is because, a business running across the years has stock carried over from previous years; it is not so easy as to only deduct sales from purchases. The question here is: What was the cost of stock that was sold during the year? To find this, what we do, is that we add the net purchases made during the year to the opening stock and subtract the total from the closing stock. The end-figure is what is often referred to as “Adjusted Purchases”, which together with Direct expenses, comprises the “Cost of Goods Sold”.

Note: Whenever I say Net Purchases, it refers to the purchases net of purchase returns i.e., Net Purchases = Purchases – Purchase Returns.

The Birth

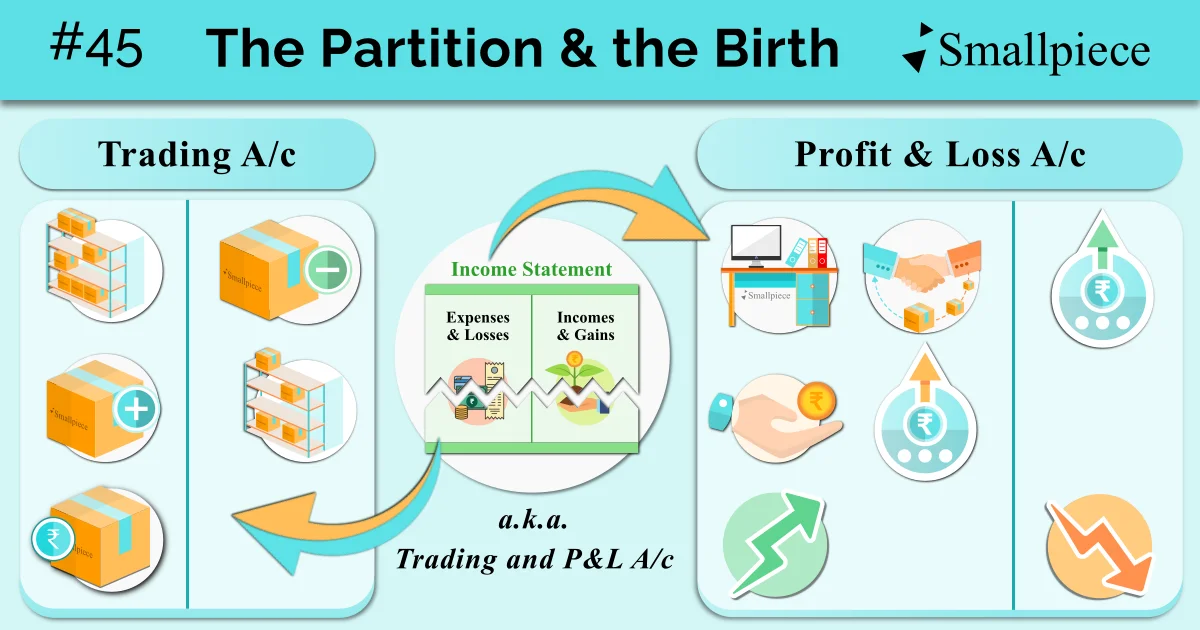

With the separation of expenses and the naming of the profit levels, the partition of Income Statement followed. The part till the calculation of Gross Profit / Loss came to be known as the “Trading and Manufacturing Account”. Now, for the sake of simplicity, let us exclude factory expenses for the time being and just think of a normal trading business, in which case it becomes only the “Trading Account” whose purpose is to ascertain profit generated from the trading activities of the business.

The part, including indirect expenses, losses and other income to arrive at the net profit came to be known as the “Profit & Loss Account” whose purpose is to ascertain the final profit, attributable to the owner(s).

With the partition of this Income Statement into Trading Account and Profit & Loss Account, the merged statement, is also referred to as Trading and Profit & Loss Account in various accounting texts.

It is at this moment where we end our discussion. Do find a summary of this partition in the graphics that follow.

Summary Graphics

Academic Reference

NCERT Class 11 Accountancy, 2026-27 Reprint, Chapter 8 Financial Statements-I, Topic 8.4.3

https://ncert.nic.in/textbook.php?keac2=1-2

Leave a Reply