After having a brief introduction to Trial Balance, it is now time to find an answer to the second issue.

Context

In our part 02 of Chintan Shivir, we came up with three issues:

First: Just like how Ledger acts as some sort of a check over journal, shouldn’t Ledger also have some sort of checking mechanism before we move to our P&L calculation?

Second: In addition to our one-page P&L calculation, wouldn’t it be better if we had a list of all our debtors-creditors or at least a total of their dues at one place as well? In short, we must know the position of a business in relation to its receivables & payables.

Third: It is good that we include our receivables and payables in our accounting system. But, shouldn’t we put a little more emphasis on cash? In our calculation, we got a loss of ₹9,925 but our cash balance, as we can calculate from our Ledger accounts, is ₹51,350 (i.e., 1,13,250 – 61,900).

Discussion

The answer to the first issue was Trial Balance.

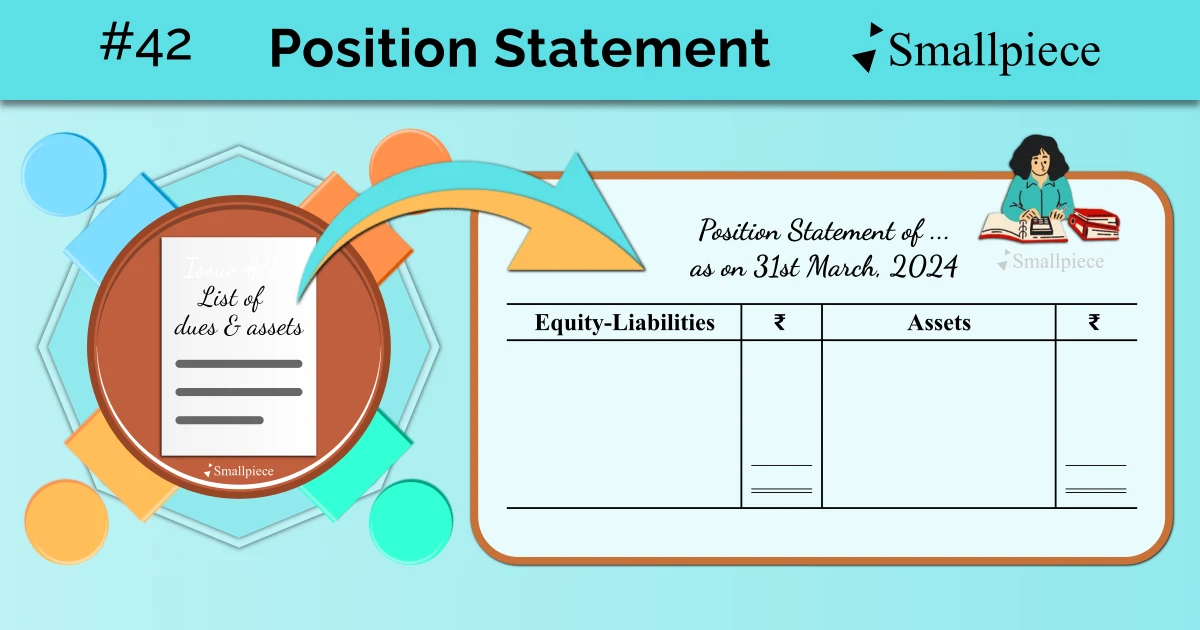

To resolve the second issue, we can use a specific kind of layout where we can list creditors on one side (say, the left side) and debtors on the other (i.e., the right side).

As with all types of layouts, we must also think of what to call this layout and the headers for the columns. To do so, I ask that you recall the 4 types of transactions / accounting items: Equity-Liabilities, Assets, Incomes and Expenses.

Creditors, by nature, refer to obligations that a business must fulfill and thus, fall under the synonymous category of Equity-Liabilities, which becomes our first header.

On the contrary, Debtors fall under the blanket category of Assets, which will be our second header.

As for the title of the layout, since we are using it to know the “position” of the receivables & payables, we can just call it the “Position Statement”.

Using this layout, on one side, we have a list for Equity-Liabilities through which we get a total amount due to the creditors and on the assets side, we have a total amount that is due from the debtors.

In addition, since our column headers are both two major “categories” of accounting items, we must also bring the other items from our Trial Balance that fall under them.

On the Equity-Liabilities side, we also include items like Owner’s Capital, Retained Earnings / Loss, Incomes received in advance, etc.

And, on the Assets side, all other assets like furniture, cash, prepaid expenses, etc. will be included.

With these additions, this layout not only shows the position of its receivables-payables, but all its other liabilities & assets providing a snapshot of whether the business has been able to generate profit or not, the sources of funds employed and their use to acquire the various assets.

And thus, I believe, we’ve found a satisfactory solution to the second issue brought up in our Chintan Shivir, which is the Position Statement, marking the end of today’s discussion.

Leave a Reply