It is now time that we explore our second financial statement: the Position Statement or what the accounting world calls the “Balance Sheet”.

Layout

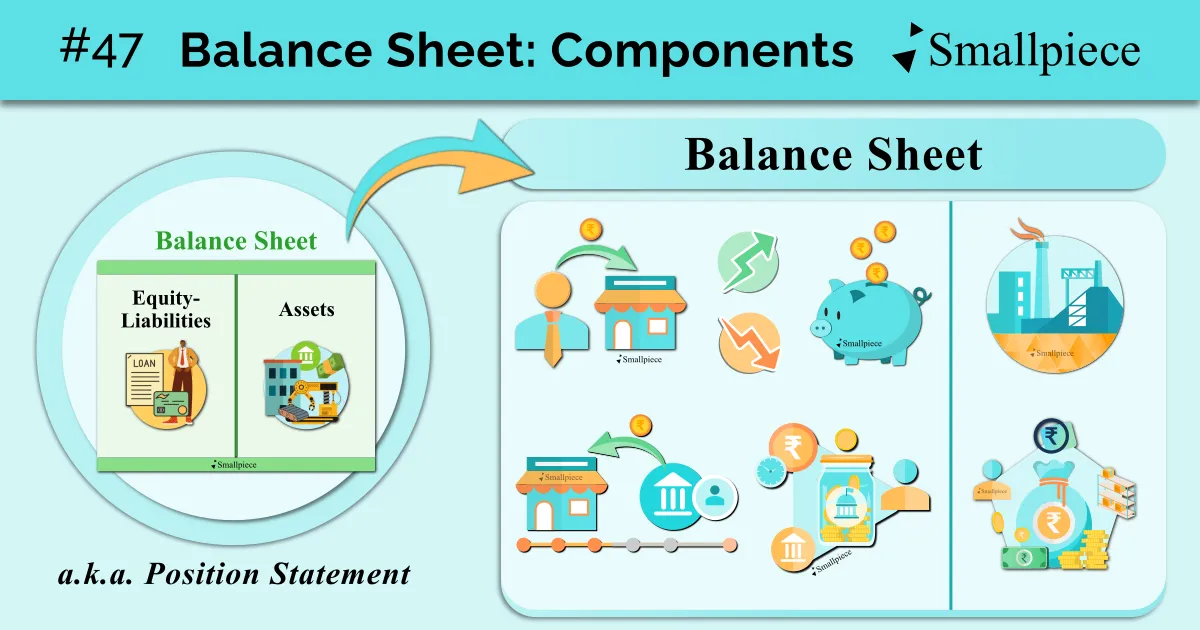

Balance Sheet, just like Income Statement, is divided into two sides: one for Equity-Liabilities and the other for Assets.

Components

Let us begin from the left: the Equity-Liabilities side. As the column header suggests, this side records:

(A) Owners’ funds or Equity i.e., what the business owes to its owners and

(B) Outside Liabilities i.e., what it owes to banks, creditors, etc.

Equity, first of all, includes Capital i.e., the money invested by the owner(s) into the business. Profit / Loss for the year that has resulted from this capital naturally belongs to the owner and is added to / subtracted from the same. On the other hand, any drawings made during the year have to be deducted.

Then come the Liabilities, which are further divided into two categories based on their time period.

The liabilities which have to be fulfilled over a series of accounting years are termed as “Non-Current Liabilities”.

These usually include long-term loans or borrowings of any kind, be it formal loans from banks or informal borrowings from friendss.

While, those liabilities which have to be fulfilled within 12 months i.e., before the end of next accounting year are termed as “Current Liabilities” (e.g., short-term loans, creditor dues, advance income, outstanding expenses, etc.).

Now, coming to the right side of the Balance Sheet: the Assets side.

Assets, too, are further classified into: Non-Current and Current based on their time period.

Non-Current Assets, i.e., assets remaining in the business over a series of years, include land & building, plant & machinery, patents & copyrights, long-term investments, etc.

Current Assets include stock, cash, bank balance, debtors, short-term investments, prepaid expenses, receivable incomes, etc.

Where do Reserves & Provisions, the categories we last discussed, fall in?

Reserves, as we last saw, are also called ‘Undistributed Profits’.

Despite being undistributed, they are still profits and are ultimately, placed together with Capital and other Equity items.

Provisions, on the other hand, are created to cover expected decline in an asset item. For e.g., bad debts & discount represent a decline in debtors while depreciation represents a decline in the value of the concerned asset. Thus, they are recorded as a deduction to the respective asset account they are tied to, with one exception: Provision for tax, which represents a future ‘liability’ to the government and usually comes under “Current Liabilities”.

With this last item, we’ve completed our overview of the layout & components of the Balance Sheet. Find a small summary of this layout as follows:

Next, we’ll discuss the formal procedure of recording our accounting items under the layouts of the Income Statement and the Balance Sheet.

Academic Reference

NCERT Class 11 Accountancy, 2026-27 Reprint, Chapter 8 Financial Statements-I, Topic 8.6

https://ncert.nic.in/textbook.php?keac2=1-2

Leave a Reply