As promised in the last meeting, here, we’ll discuss how to include the balance figure in the account space.

The answer lies in a single word: “Doppelganger”, synonymous to clone, body-double, or better, a “Duplicate”.

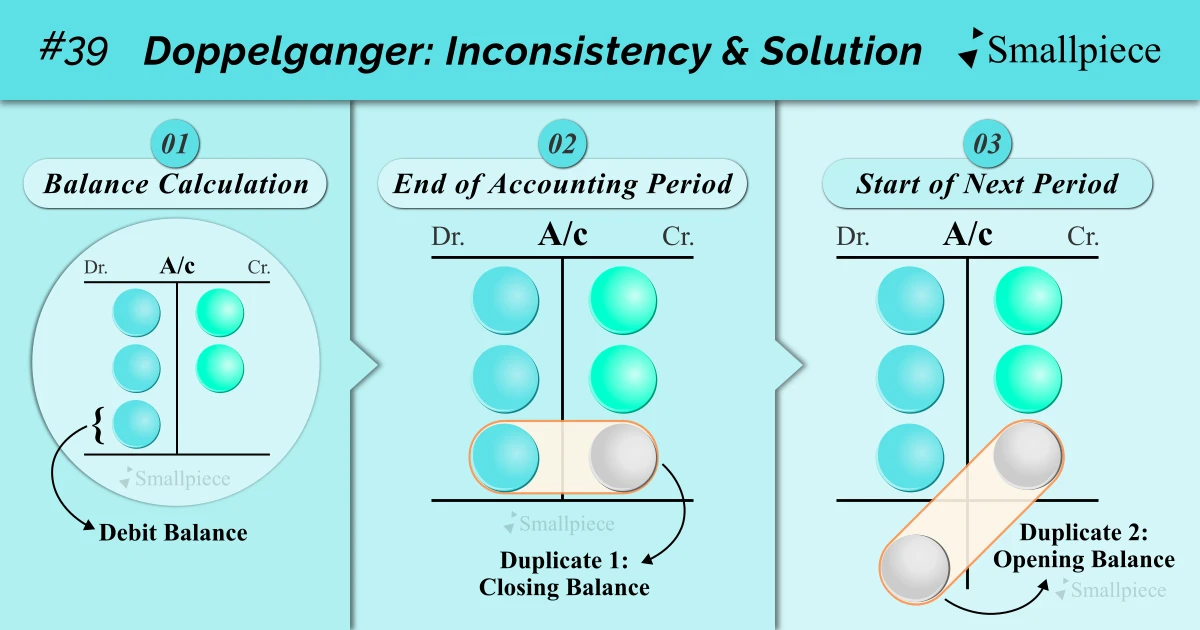

The creators of our accounting system found it wise to simply duplicate the balance on the smaller side.

This resulted in:

- Both debit & credit sides being equal (at least in the T-Account space) and,

- Enabled the accountant and/or owner to take a quick glance at the balance of any account at any given time without the hassle of recalculation.

Now, our cash account would look something like this:

However, this idea created a conflict with the Dual Aspect Concept or the Equality of Debits & Credits overall.

Recall that whenever we gave debit & credit tags in journal entries, their totals always tallied i.e., for every debit effect, there must be a credit effect and vice versa.

By duplicating the balance for our convenience, we’ve given birth to one effect out of thin air without its corresponding effect which violates the equality of debits & credits overall.

So, what to do? Do we need to learn some specialized entry to deal with this?

Nope! The answer this go around comprises of two words: “ONCE MORE!”

Just duplicate the balance once more on its original side and then, lo and behold! the equality of debits & credits is upheld.

Simple. No need to make additional entries in journal, whatsoever.

Closing Balance & Opening Balance

To give more relevance to this plain concept of cloning / duplicating balance, it is often tied to a specific timeframe: end of an accounting and beginning of the other.

Our cash balance of ₹51,350 was calculated on 31st March i.e., at the end of A.Y. 2023-24 and is thus, called “Closing Balance” of cash account as at this date.

This cash, of course, won’t vanish and is expected to stay in the business, which is why it will be carried forward to the accounting records of the successive A.Y. 2024-25 as “Opening Balance”.

In other words, on 1st April, the cash account will open with the balance of ₹51,350 from previous year.

And that is it for today. Next, before learning new things, we’ll take a step back, ponder on the learnings till now and see, if there’s any more queries / issues we need to address. Do read the upcoming Chintan Shivir #02.

For practice, navigate to the references section for the NCERT resource, make journal entries and create ledger accounts with balances.

Reference

1. NCERT Class 11 Accountancy (2026-27 Reprint) Chapter-3 Recording of Transactions-I

https://ncert.nic.in/textbook.php?keac1=3-7

Leave a Reply