A little recap: In our last meet, we discussed the drawbacks of calculating P&L from journal and the spawn of ledger to ease this process by grouping transactions / entries relating to an item at one place (say, the outgoing and incoming of cash due to various reasons are grouped at one place which gives us the net cash left for easier calculations moving forward)

In here, we’ll learn what the term ‘account’ actually stands for now that we are acquainted with Ledger.

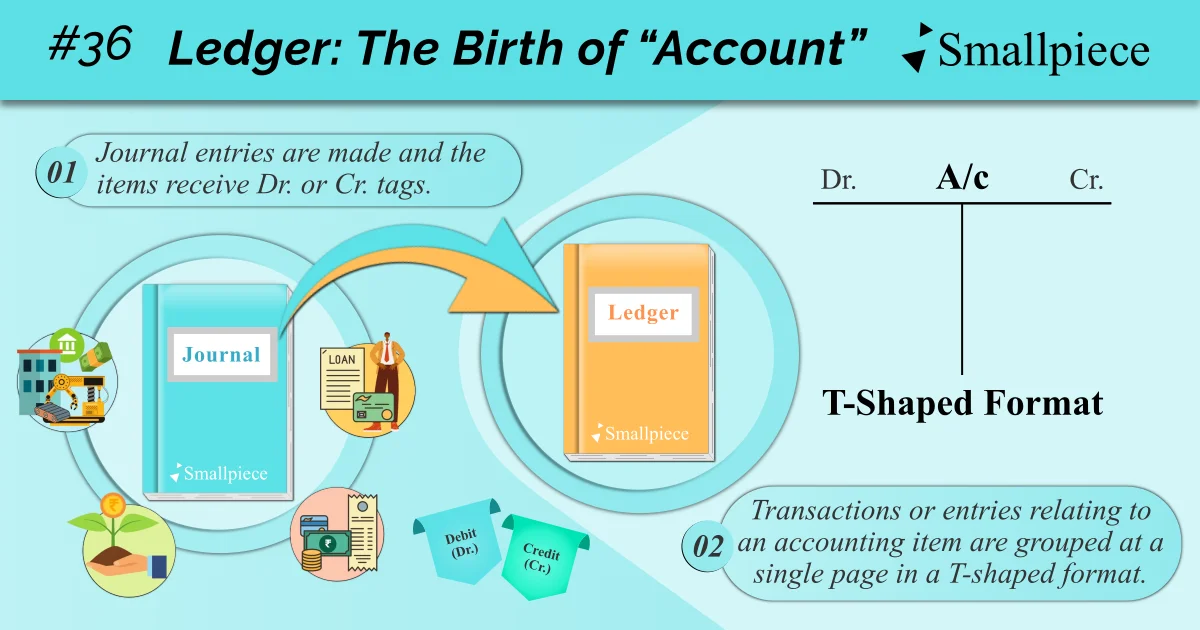

The purpose of this secondary book, once more, is to group similar items or, transactions relating to the same items.

To do so, a T-shaped layout was finalised as follows:

To understand this better, why don’t we take the example of the ‘cash’ item.

Journal entries that involve cash item will be brought into a T-shaped space on a specific page, effectively creating a grouping of transactions relating to the cash item which makes calculations easier.

On the left side, we’ll list those transactions where Cash item has received the debit tag i.e., transactions where cash has decreased.

And, on the right, those transactions will be listed where Cash item has received the credit tag i.e., where cash has increased.

At the end, a total of both sides is calculated from which we can determine how much cash we have left on our hands.

This side-by-side grouping of similar items with their respective Dr. & Cr. tags on the same page in ledger is what we infamously call an “Account”.

The concept of Ledger brings two new things in our accounting practices: (1) Posting and (2) Ledger Folio, which is what we will discuss next.

Till then, if you wish to explore how ledger is taught academically, go to the NCERT resource linked in the reference section.

A Side Note – the suffix A/c in Journal Entries

If you’ve noticed, before introducing ‘Account’ in this discussion, I’ve continuously avoided using the term, despite our subject being “Accounting”.

My only purpose, if you’re new to the subject, was to save you from the headache that all commerce students (including myself) had to go through not knowing the true meaning of account: a simple grouping of transactions relating to a particular accounting item.

Our confusion was attributable to one more thing I’ve kept from you till now.

While making journal entries, the suffix ‘A/c’, short for Account is almost always added to any item in journal entries. For instance, we’ve used the item Cash many times in our discussion on journal entries. In reality, owing to the use of ledger, we use not Cash but Cash A/c while making an entry, indicating that the entry is to be posted in the Cash Account in Ledger. This is also the case for all other items.

This makes sense only after one is sequentially introduced to journal and then, ledger. Unfortunately, my generation didn’t have that luxury and surprisingly, even the present commerce students don’t.

Interestingly, for whatever reason, there is one exception where you can get away without using the suffix ‘A/c’ but knowing it is only optional. If you wish, view the document linked in the resources / references section below.

Resources / References

1. NCERT Class 11 Accountancy Chapter 3 Recording of Transactions-I, pg. 27 onwards

https://ncert.nic.in/textbook/pdf/keac103.pdf

2. Exception to the ‘A/c’ suffix:

Leave a Reply