Just like how ledger postings first require a journal entry, any sort of recordings in our financial statements, particularly the Income Statement, require a entry of their own, called the “Closing Entry”.

Why the word “Closing”? Because incomes & expenses, which form the two sides of the Income Statement, are confined to the boundary of the financial year. The balances in accounts coming under these categories must always be squared-off i.e., accounts closed, on 31st March, the end date.

And how do we close these accounts? By making an entry in Journal, our primary book of accounting.

This entry should remove the balance from the respective accounts and place them at their rightful positions in the Income Statement.

Suppose, after deducting returns, there is a debit balance of ₹15,000 in the Purchases account.

To close or square-off this account, we need a credit effect equaling this amount. Hence, in the closing entry, Purchase a/c will be credited and as for debit, it will be the Income Statement.

Through this entry, we are in effect, transferring the balance of ₹ 15,000 in purchases to the debit side or the “Expenses & Losses” side of the Income Statement, which is its rightful place in the financial statements.

For items belonging to the Incomes & Gains category, the item concerned will be debited and the Income Statement should be credited.

However, at this point, we must recall that the Income Statement had undergone a partition resulting in the birth of the Trading A/c and the Profit & Loss A/c.

Thus, instead of “Income Statement”, we’ll have to use Trading A/c or Profit & Loss A/c based on the accounting item concerned.

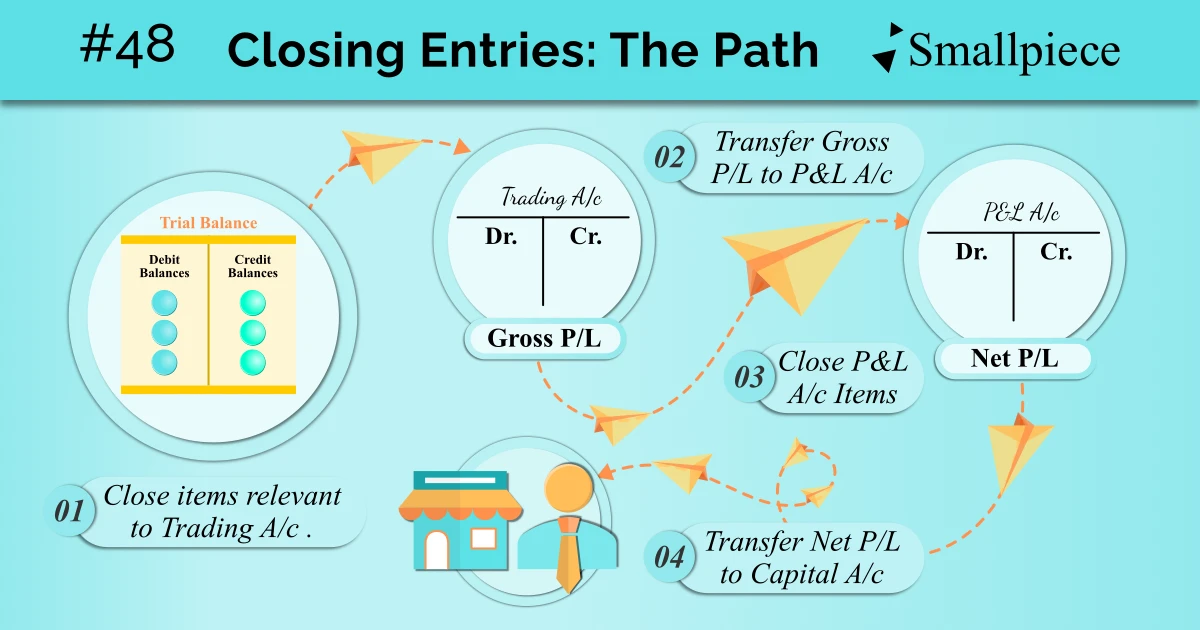

When all relevant items have been brought into the Trading A/c, this account too is closed by transferring its balance (Gross Profit / Loss) to the Profit & Loss A/c. Then, the balance of P&L A/c (Net Profit / Loss) is usually transferred to the Capital A/c, after provisions and/or reserves have been filled.

Closing Entries – Trading A/c

Let us bring the summary graphic of trading account here.

Closing entries to bring the necessary items into the trading account are as follows, where the returns (be it purchases return or sales return) are first closed into Purchase and Sales Account, after which the other entries are made to bring the prescribed items to the Trading Account, except Closing Stock.

Closing Entries for Trading Account

1. Purchases Return

Purchases Return A/c

Dr.

To Purchase A/c

2. Sales Return

Sales A/c

Dr.

To Sales Return A/c

3. Opening Stock, Purchases and Direct Expenses

Trading A/c

Dr.

To Opening Stock A/c

To Purchases A/c

To Direct Expenses A/c

4. Sales

Sales A/c

Dr.

To Trading A/c

5(A). Transfer of Gross Profit (credit balance of Trading A/c) to P&L A/c

Trading A/c

Dr.

To Profit & Loss A/c

5(B). Transfer of Gross Loss (debit balance of Trading A/c) to P&L A/c

Profit & Loss A/c

Dr.

To Trading A/c

After all relevant items have been recorded, the Gross Profit / Loss is found, which is nothing but the balance of the Trading Account. Then, this account is closed by transferring its balance to the Profit & Loss Account

Secondly, you must have noticed that there’s no entry for closing stock. While it also a part of Trading A/c, the entry for the same which will be covered later on.

Closing Entries – Profit & Loss A/c

Just like Trading Account, let us first remember what items are included in the Profit & Loss Account from the summary graphic below.

After the Gross Profit / Loss has been brought over from the Trading Account, closing entries to bring accounting items belonging to the concerned categories in the Profit & Loss Account are made as under.

Closing Entries for P&L Account

1. Expenses & Losses categories included in P&L A/c

Profit & Loss A/c

Dr.

To Office & Admin Expenses A/c

To Selling & Distribution Expenses A/c

To Financial Expenses A/c

To Other Expenses & Losses A/c

2. Incomes & Gain categories included in P&L A/c

Other Incomes & Gains A/c

Dr.

To Profit & Loss A/c

3(A). Transfer of Net Profit (i.e., credit balance of P&L A/c) to Capital A/c

Profit & Loss A/c

Dr.

To Capital A/c

3(B). Transfer of Net Loss (i.e., debit balance of P&L A/c) to Capital A/c

Capital A/c

Dr.

To Profit & Loss A/c

At the end, the balance of P&L Account is found as well, which is what we call the Net Profit / Loss. This is transferred to the owner’s Capital Account and the P&L Account is thus, closed.

In summary, the path of closing entries may be traced and represented as follows:

Academic Reference

NCERT Class 11 Accountancy, 2026-27 Reprint, Chapter 8 Financial Statements-I, Topic 8.4.2

https://ncert.nic.in/textbook.php?keac2=1-2

Leave a Reply