In our pursuit of streamlining calculations, the concept of balance proves to be a worthy ally.

We are aware that any item, be it an Asset, Liability, Expense or Income can receive both the debit & credit tags.

Secondly, its account in Ledger gives us a complete list of when & why it received those tags.

What follows is the concept of balance.

Balance: Meaning

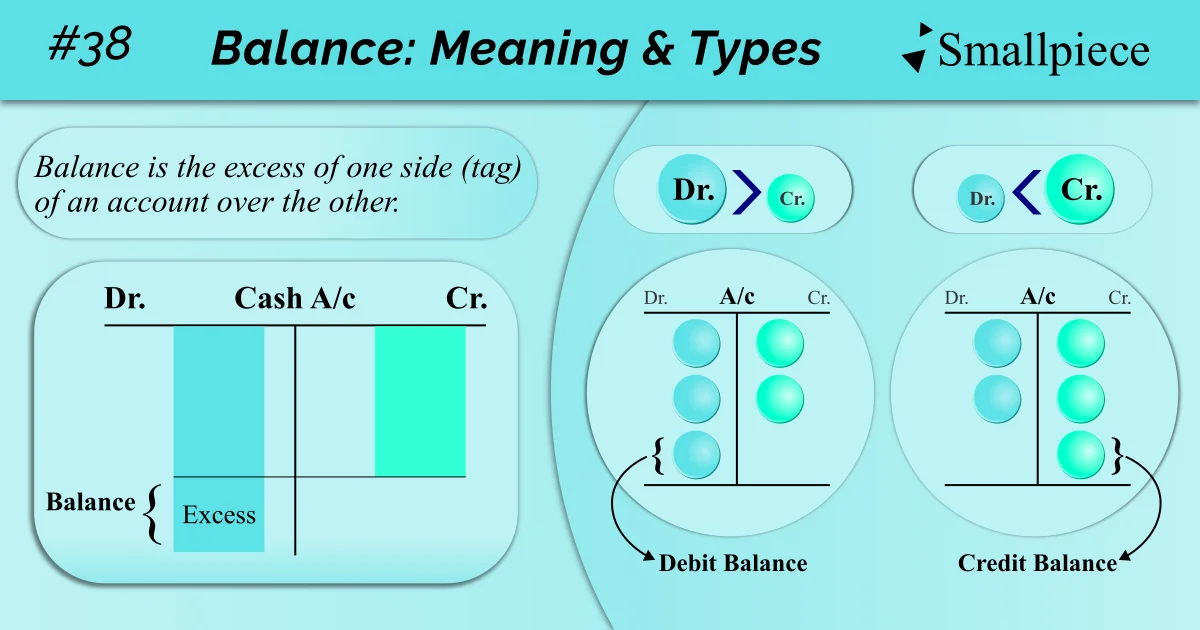

Put simply, it is the excess of one tag over the other in a particular account i.e., it is the net result of the calculations in a particular account.

To aid better understanding, let us bring the cash account from the ledger of Hitesh Traders.

Here, the debit side (i.e., the cash receipts) is larger at ₹1,13,250 compared to the credit side (i.e., the cash payments) at ₹61,900 and the ‘excess’ of debit over credit is ₹ 51,350 which is the cash left at hand. This excess, in accounting jargon, is called balance.

Types of Balance

Depending on which tag is bigger, balance is categorised into:

1. Debit Balance:

With reference to total amount, when the debit tag or rather, the debit side of a T-account is larger, the balance is referred to as Debit Balance.

2. Credit Balance:

The opposite of debit balance, when the credit tag or rather, the credit side of a T-account is larger, the balance is referred to as Credit Balance.

In the above example of Cash Account from the Ledger of Hitesh Traders, for the sake of classification, it is said to have a debit balance of ₹51,350.

Benefits of Calculating Balance

Key benefits include:-

- Netting – As seen in the example of cash account, balance is the net of calculations in a T-account. It saves the hassle of going through all entries in an account when needing answers to basic queries like “How much cash do we have left?”, “How many of our creditors still need to be paid?” or “How much debt is still left to be repaid?” that any business needs answers to from time to time.

- Summary / Snapshot – Making a list of the various balances will help provide a summary of the business position at a certain point of time as to how much liabilities in the form of creditors & loans are still left to be discharged and how does the business fare with respect to the assets it possesses at present that will help generate income to discharge these liabilities & maintain profit.

A Problem

In this little talk we’ve had, there is a small problem, that of ‘Isolation’.

We’ve calculated the net figures ‘outside’ of the T-Account space. If we want to keep on monitoring an item and its balance, we need to recalculate the net figures time & again as the need arises. It is tedious to take up a calculator each time the need arises.

Secondly, if I were to slightly tweak the nature of my query from “How much cash do we have left?” to “From where have we generated cash against payments made and how much is left at the moment?”, the concept of isolating balance from the account space doesn’t make much sense. We need a workaround to somehow include this net figure in the account space itself.

Resolving this problem is something that we’ll discuss next.

Leave a Reply